Fannie and Freddie allow Vantage Score 4

Summary:

The provided texts announce a significant shift in the U.S. mortgage market, as the Federal Housing Finance Agency (FHFA) has authorized Fannie Mae and Freddie Mac to accept VantageScore 4.0 for mortgages, effective immediately. This decision aims to increase competition in the credit scoring ecosystem, previously dominated by FICO, and potentially lower costs for consumers. VantageScore 4.0 is presented as a more inclusive model, capable of scoring millions more Americans by considering alternative data like rent payments and placing less emphasis on medical collections or older tax liens, thereby expanding access to homeownership for “thin file” or underserved borrowers. While the tri-merge credit scoring model will remain, this change is expected to revolutionize mortgage underwriting, offering lenders lower costs and simplified transitions without requiring new infrastructure.

Visualization:

Explore visual by clicking on each bar

|

|

|

|

|

|

|

|

|

|

|

|

|

Main Theme and key Findings:

Expand each topic to read more

Key Points:

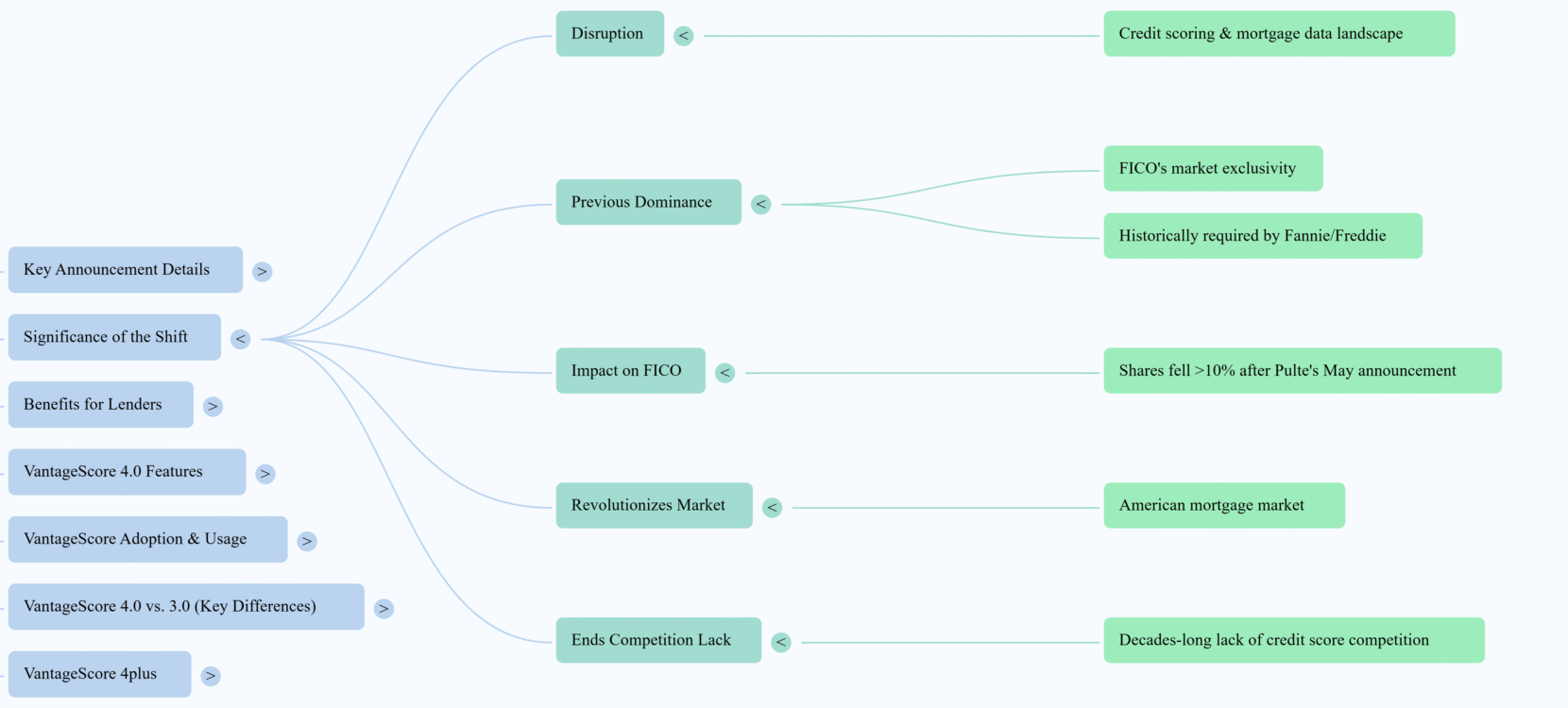

- Increased Competition in the Credit Scoring Market:

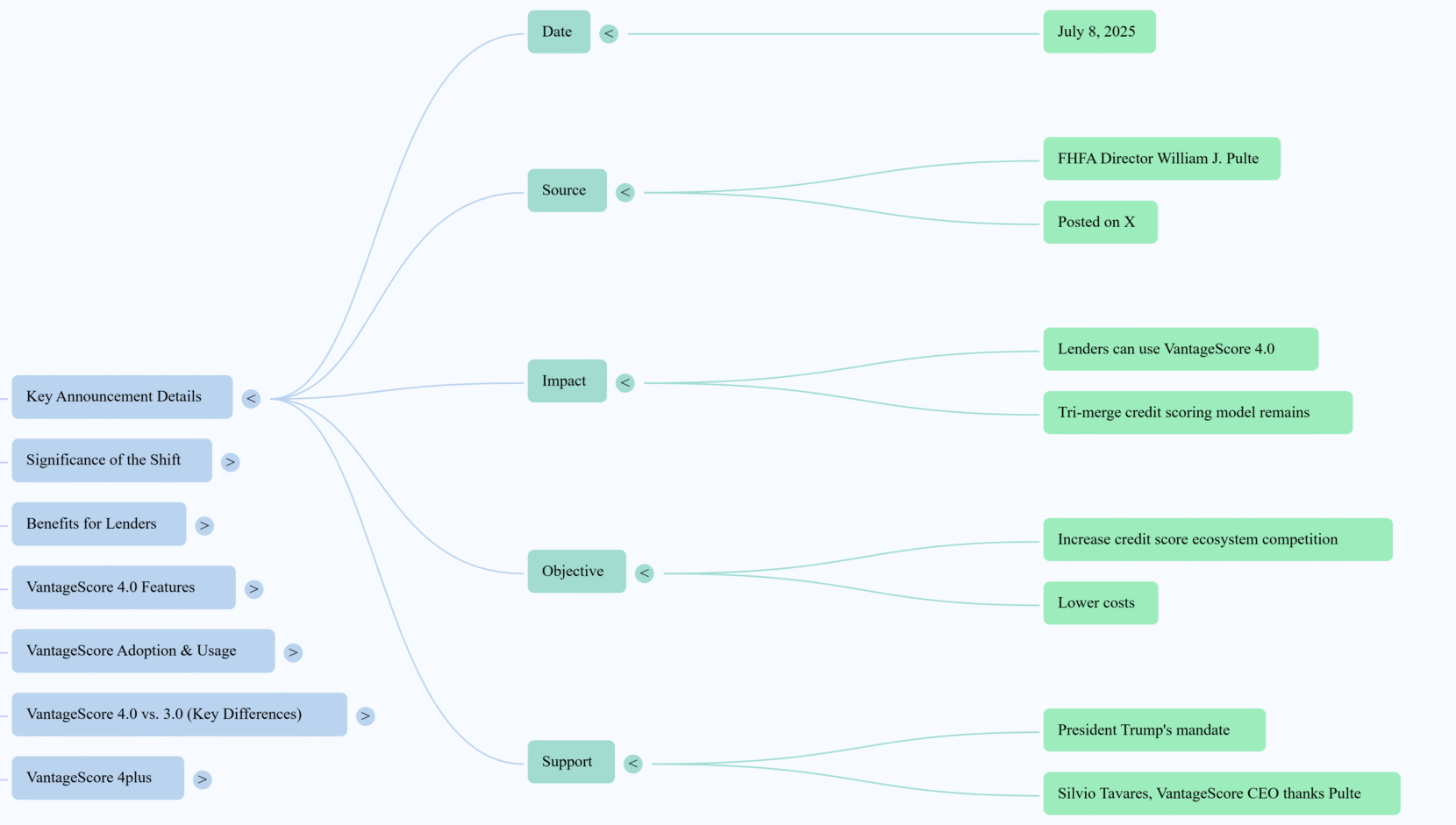

- The primary stated goal of the FHFA’s decision is to foster competition in the credit score ecosystem. Director Pulte explicitly stated, “to increase competition to the Credit Score Ecosystem and consistent with President Trump’s landslide mandate to lower costs, Fannie and Freddie will ALLOW lenders to use Vantage 4.0 Score with no current requirement to build new infrastructure (stays Tri Merge).”

- VantageScore’s President and CEO, Silvio Tavares, echoed this, stating the announcement “ends a decades-long lack of credit score competition in the U.S. mortgage market.”

- This move directly impacts FICO’s near-exclusive position in the mortgage underwriting process, as Fannie Mae and Freddie Mac previously required FICO scores. Shares of FICO reportedly fell over 10% following Pulte’s announcement.

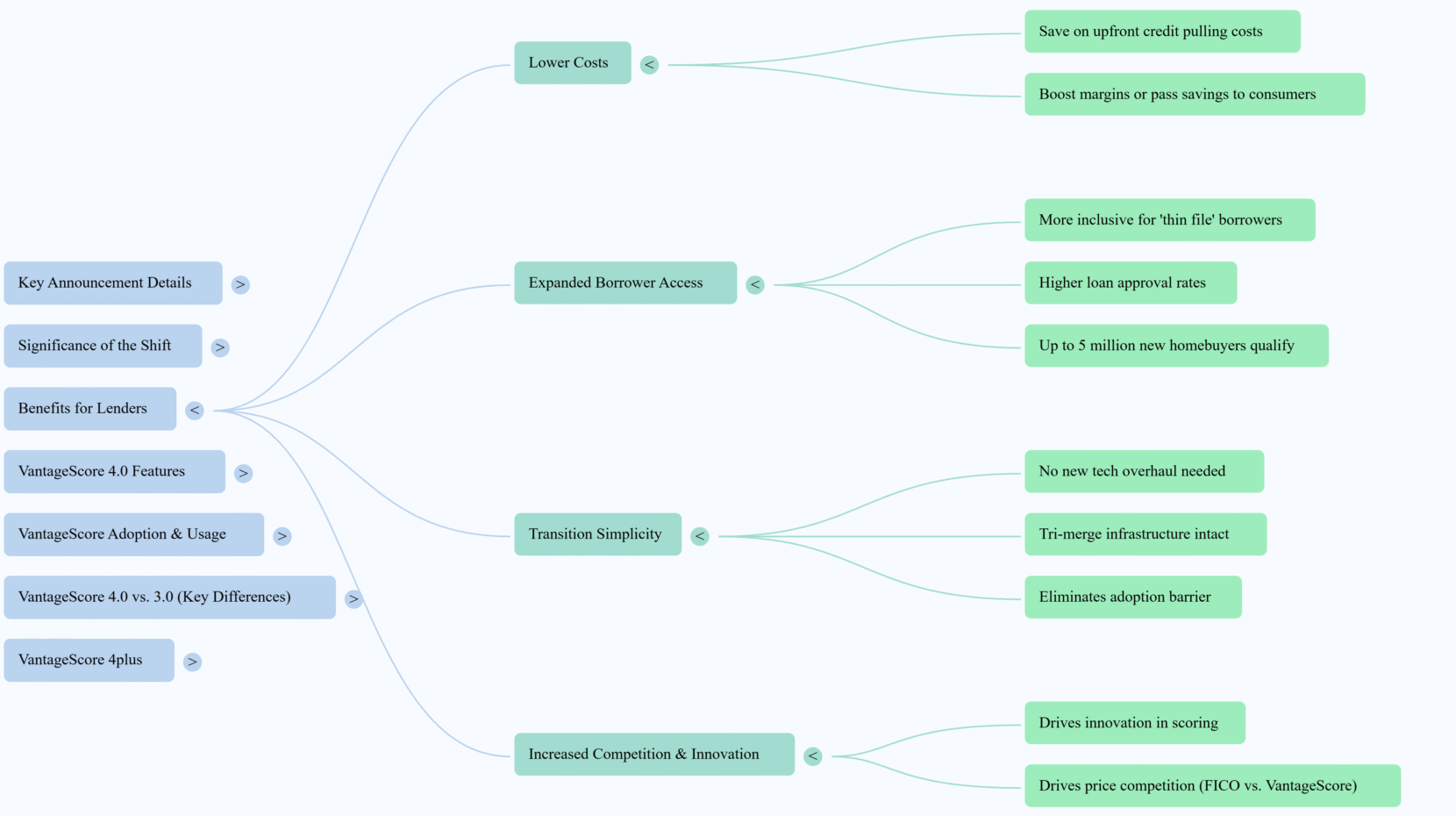

- Expanded Credit Access and Financial Inclusion:

- A major benefit highlighted is the expansion of credit access to a broader segment of the population. Pulte emphasized this, stating, “We are expanding credit access to millions of forgotten Americans — people who live in rural areas, renters who pay their rent on time every month — and bringing down closing costs.”

- VantageScore 4.0 is designed to be more inclusive, particularly for “thin file” borrowers or those with limited credit history. The model’s innovative incorporation of “alternative data sources like rent, utility, and telecommunications payments” is key to this.

- According to VantageScore, this change could enable “up to five million more prospective homebuyers” to qualify for a home purchase. It also “eliminates the requirement for recent credit activity,” benefiting groups like active and recently retired military members, and removes the “requirement for the consumer credit file to be older than 6 months,” aiding “previously underserved, young-to-credit Americans.”

- Director Pulte specifically noted, “My ORDER today (thanks to my boss, POTUS) will allow for Americans to use their RENT to qualify for a mortgage… Credit history will no longer just include credit cards and loans. This is HUGE.”

- Potential for Lower Costs and Increased Efficiency:

- The FHFA’s decision is expected to lead to “lower costs” for both lenders and consumers. If VantageScore licensing costs are lower than FICO, lenders could save on upfront costs during loan origination, potentially boosting margins or leading to savings passed on to consumers.

- VantageScore projects “up to $1 Trillion in Incremental Mortgage Activity” as a result of this policy change.

- The “Transition Simplicity” is also a key factor, as the existing “tri-merge infrastructure remains intact, no new tech overhaul is needed.” This eliminates a significant barrier to adoption for lenders.

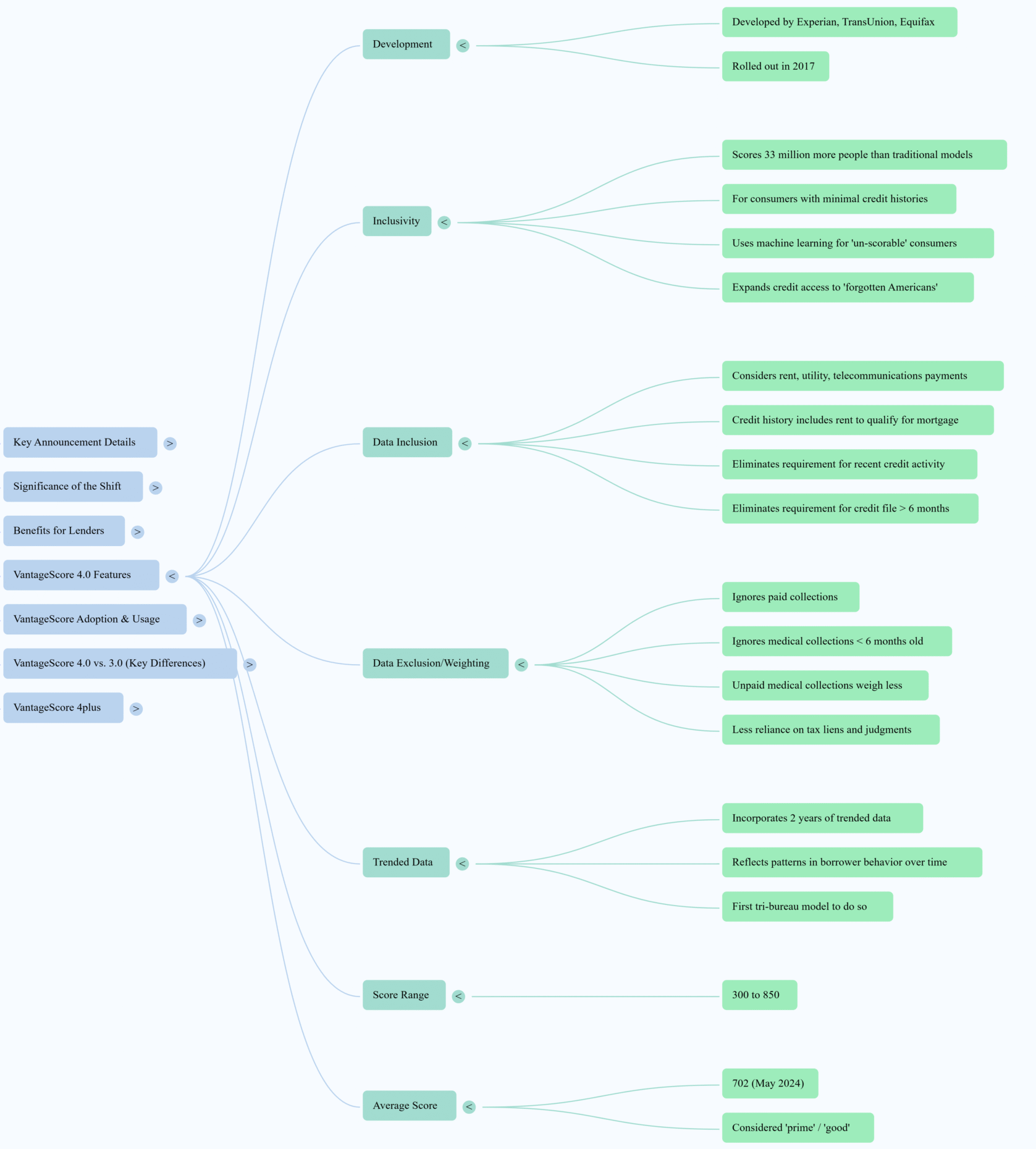

- VantageScore 4.0: Model Attributes and Usage:

- VantageScore 4.0 was developed by the three major credit bureaus (Experian, TransUnion, and Equifax) and rolled out in 2017.

- Its “main selling point is that it uses machine learning to help provide scores for consumers with minimal credit histories or thin credit files.” It can score “about 33 million more people than traditional models.”

- Unlike some older models, VantageScore 4.0 “doesn’t use paid collections or medical collections in its calculations.” It also “ignores medical collection accounts that are less than six months old.”

- A significant feature is its use of “trended credit data,” which factors in “shifting credit behaviors over time” rather than just a single point in time. This includes how utilization rates evolve over up to two years.

- The average VantageScore 4.0 is 702 as of May 2024, considered a “prime” score.

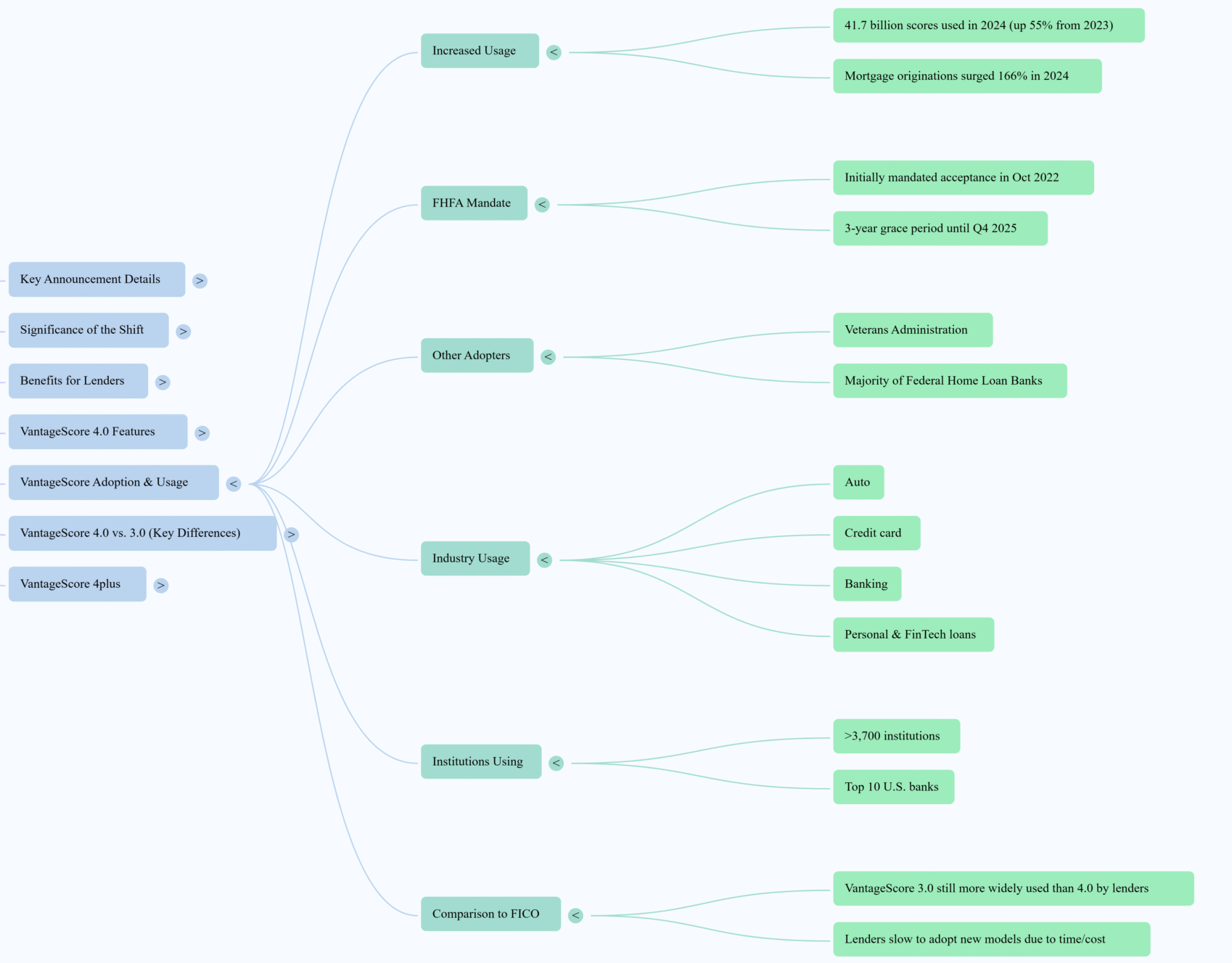

- Usage of VantageScore has seen substantial growth, with 41.7 billion VantageScore credit scores used in 2024, a 55% increase from 2023.

- Implementation and Context:

- The FHFA’s announcement follows a 2018 Credit Score Competition Act, signed by President Trump, which established the use of modern credit scoring models for GSE mortgages.

- The FHFA initially mandated acceptance of VantageScore in October 2022, providing a three-year grace period. Other federal entities like the Veterans Administration and several Federal Home Loan Banks have already adopted VantageScore 4.0.

- While the immediate implementation is expected to be smooth due to the “tri-merge” model remaining, some “doubts arise regarding potential changes that may be needed to move to VantageScore credit scoring,” indicating potential future considerations for lenders.

- Director Pulte views this as part of a broader mandate to “lower costs” and improve outcomes for American consumers, referencing President Trump’s “landslide mandate.”

- In conclusion, the FHFA’s approval of VantageScore 4.0 marks a pivotal moment for the U.S. mortgage market. It promises to increase competition, reduce costs, and significantly broaden access to homeownership for millions of Americans by embracing a more inclusive and modern credit scoring methodology.

Question and Answer:

What significant announcement did FHFA Director William J. Pulte make on July 8, 2025, regarding Fannie Mae and Freddie Mac?

- Director Pulte announced that lenders working with Fannie Mae and Freddie Mac are now permitted to use VantageScore 4.0 for mortgage credit scoring. This decision aims to increase competition within the credit score ecosystem and reduce costs for consumers, while still allowing lenders to maintain a tri-merge credit-scoring model.

How does the adoption of VantageScore 4.0 by Fannie Mae and Freddie Mac impact FICO’s historical market position in mortgage underwriting?

- FICO has historically held a dominant and exclusive position in mortgage underwriting, especially with Fannie Mae and Freddie Mac requiring FICO scores. The FHFA’s decision to allow VantageScore 4.0 erodes this exclusivity, introducing competition and potentially leading to a loss of FICO’s market share and a decrease in its stock value.

What is “trended data” in the context of VantageScore 4.0, and how does it differ from older scoring models?

- Trended data in VantageScore 4.0 reflects patterns in borrower behavior over time, such as how their credit utilization rate trends over a period of up to two years. Unlike some older scoring models that only consider the most recently reported utilization rate, VantageScore 4.0’s use of trended data provides a more comprehensive and nuanced picture of a borrower’s credit habits.

Describe two key benefits for mortgage lenders resulting from the FHFA’s announcement to allow VantageScore 4.0.

- Two key benefits for mortgage lenders include potentially lower costs due to reduced VantageScore licensing fees, which can boost margins or be passed to consumers. Additionally, it offers expanded borrower access, as VantageScore 4.0 is more inclusive, potentially qualifying up to five million more homebuyers, especially those with “thin files” or limited credit history.

How does VantageScore 4.0 aim to expand credit access to “forgotten Americans,” particularly those in rural areas or renters?

- VantageScore 4.0 expands credit access by considering a broader range of payment types in determining creditworthiness, including rent and utility payments. This allows individuals who previously lacked extensive credit card or loan histories, such as renters who consistently pay on time or those in rural areas, to qualify for mortgages.

What was the growth in VantageScore usage between 2023 and 2024, as reported by National Mortgage Professional?

- National Mortgage Professional reported that VantageScore usage increased significantly by 55% from 26.9 billion scores in 2023 to 41.7 billion scores in 2024. This indicates a substantial rise in its adoption and use across various lending sectors.

What is the “tri-merge credit-scoring model,” and why is its continued use significant despite the allowance of VantageScore 4.0?

- A tri-merge credit-scoring model involves pulling credit data from all three major bureaus (Experian, TransUnion, and Equifax) simultaneously. Its continued use is significant because it eliminates the need for lenders to build new infrastructure, thereby simplifying the transition to VantageScore 4.0 and removing a major barrier to adoption.

How does VantageScore 4.0 treat medical collection accounts in its calculations, and what is the reasoning behind this approach?

- VantageScore 4.0 completely ignores medical collection accounts that are less than six months old, and unpaid medical collection accounts are weighted less than other types of collection accounts. This approach acknowledges that consumers may be waiting for insurance companies to pay these bills, providing a more lenient assessment.

According to VantageScore, how many additional prospective homebuyers could qualify for a home purchase if lenders utilize VantageScore 4.0?

- According to VantageScore, an estimated five million more prospective homebuyers could qualify for a home purchase if lenders adopt and use the VantageScore 4.0 service. This highlights the model’s potential to significantly broaden access to homeownership.

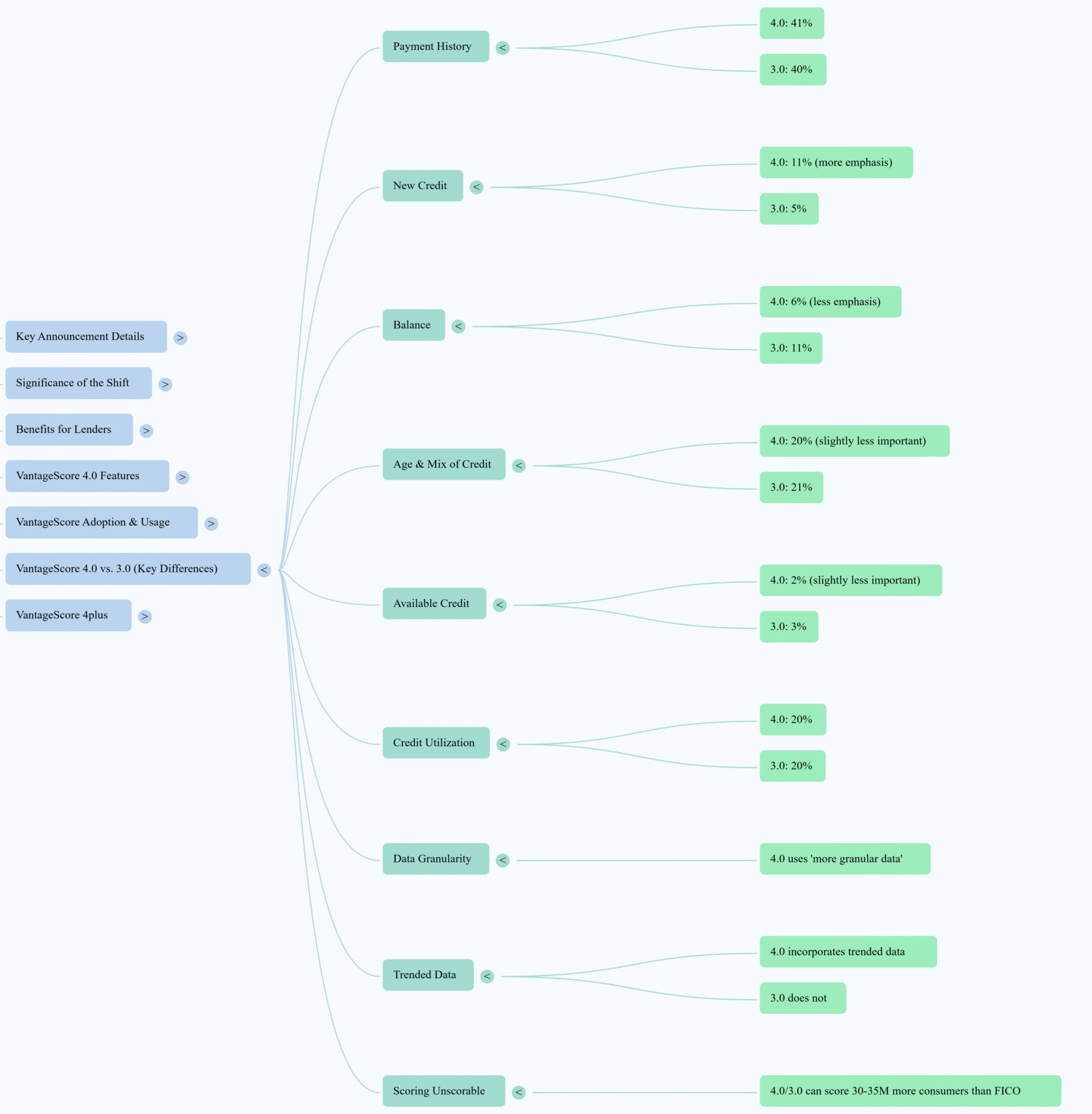

What is the primary difference in how VantageScore 4.0 calculates scores compared to VantageScore 3.0 regarding “new credit” and “account balances”?

- The biggest difference in scoring between VantageScore 4.0 and 3.0 is that 4.0 places more emphasis on “new credit,” accounting for 11% compared to 5% in 3.0. Conversely, 4.0 places less emphasis on “account balances,” at 6% compared to 11% in 3.0.

FAQs

What is VantageScore 4.0 and how does its recent approval by Fannie Mae and Freddie Mac impact the mortgage market?

- VantageScore 4.0 is one of the latest credit scoring models developed by the three major credit bureaus (Experian, TransUnion, and Equifax). Its key innovation lies in using machine learning and “trended data” (patterns in borrowing and repayment over time, including utilization rate history) to provide scores for consumers, particularly those with “thin credit files” or limited credit history. The Federal Housing Finance Agency (FHFA) recently announced that Fannie Mae and Freddie Mac, which back the majority of U.S. mortgages, can now accept VantageScore 4.0 for mortgage originations. This decision is significant because it introduces competition to a market historically dominated by FICO scores, potentially lowering costs for lenders and expanding access to homeownership for millions of Americans.

How does VantageScore 4.0 differ from previous credit scoring models, including FICO?

- VantageScore 4.0 introduces several key distinctions from older models like FICO 8 and 9, and even its predecessor, VantageScore 3.0:

- Trended Data: Unlike some older models that primarily consider a single point in time for credit utilization, VantageScore 4.0 incorporates up to two years of historical payment and utilization trends, offering a more nuanced view of a borrower’s financial behavior.

- Inclusivity for “Thin Files”: It can score approximately 33-35 million more consumers who might not have enough recent credit history to be scored by other models, such as FICO 8 or 9 (which require an account open for at least six months and reported within the last six months). This includes people in rural areas, renters who pay on time, and active/recently retired military members.

- Treatment of Negative Marks: VantageScore 4.0 gives less weight to tax liens and judgments and completely ignores medical collection accounts that are less than six months old, recognizing that insurance payments may be pending. Unpaid medical collections also hurt less than other types of unpaid collections.

- Calculation Weighting: While still broadly similar to VantageScore 3.0, VantageScore 4.0 places a slightly higher emphasis on “new credit” and less on “account balances.”

What are the main benefits of this shift to allow VantageScore 4.0 for mortgage lenders?

- The adoption of VantageScore 4.0 by Fannie Mae and Freddie Mac is expected to bring several advantages:

- Lower Costs: If VantageScore licensing fees are lower than FICO’s, lenders could save on upfront costs during loan origination, potentially boosting their margins or allowing them to pass savings onto consumers through lower closing costs.

- Expanded Borrower Access: The more inclusive nature of VantageScore 4.0, which considers alternative data like rent and utility payments, means an estimated 5 million more prospective homebuyers could qualify for a mortgage. This helps “forgotten Americans” and those with limited traditional credit history.

- Transition Simplicity: Lenders can integrate VantageScore 4.0 while maintaining their existing “tri-merge” credit check infrastructure, meaning no significant new technological overhaul is required, which removes a barrier to adoption.

- Increased Competition and Innovation: By approving an alternative credit model, the FHFA encourages greater competition in the credit scoring industry, which could lead to further innovation in scoring methodologies and potentially price competition between FICO and VantageScore.

How will the use of alternative data, such as rent and utility payments, affect creditworthiness under VantageScore 4.0?

- VantageScore 4.0 innovatively incorporates alternative data sources like rent, utility, and telecommunications payments into its creditworthiness determination. This is a significant change because traditional credit scores primarily focused on credit cards and loans. By including these regular, on-time payments, VantageScore 4.0 aims to provide a more comprehensive and accurate picture of a consumer’s financial responsibility, especially benefiting individuals who may not have extensive traditional credit histories but consistently pay their bills. This inclusion is a major factor in expanding credit access to millions who were previously underserved.

What does “tri-merge credit scoring model” mean in the context of this announcement?

- The “tri-merge credit scoring model” refers to the long-standing practice of mortgage lenders pulling credit data from all three major credit bureaus: Experian, TransUnion, and Equifax. Even with the allowance of VantageScore 4.0, lenders will continue to use this tri-merge approach. This means that while they now have the option to use VantageScore 4.0 (which itself is developed by these three bureaus), they will still obtain information from all three sources to form a comprehensive view of a borrower’s credit profile, rather than relying on a single bureau’s data or a completely new system. This continuation of the tri-merge infrastructure simplifies the transition for lenders.

What has been the trend of VantageScore usage prior to this announcement?

- Before the FHFA’s recent announcement, the usage of VantageScore had been on an upward trend. In 2024, approximately 41.7 billion VantageScore credit scores were used, marking a substantial 55% increase from 26.9 billion in 2023. While its use in mortgage originations surged by 166% in 2024, this growth was somewhat offset by a “pullback in use by the government-sponsored entities (GSEs), Fannie Mae and Freddie Mac,” due to their previous requirement for FICO scores. The FHFA’s recent decision is expected to significantly change this, removing the barrier to widespread VantageScore adoption by the GSEs.

How might this policy change impact FICO, the previously dominant credit scoring provider in the mortgage market?

- The FHFA’s decision could significantly disrupt FICO’s long-standing market exclusivity in mortgage underwriting, especially with Fannie Mae and Freddie Mac. FICO has historically dominated this process, with its scores being a requirement for mortgages sold to these GSEs. The allowance of VantageScore 4.0 erodes this exclusive position, introducing direct competition. Following initial hints of this change, shares of FICO had already fallen by more than 10%. This shift is expected to drive price competition and potentially force FICO to innovate its own scoring methodologies to maintain its market share.

What is the average VantageScore 4.0 score, and what does it indicate?

- As of May 2024, the average VantageScore 4.0 consumer credit score was 702. According to VantageScore’s ranges, a score of 702 is considered a “prime” score, which is one tier below the highest range. Generally, a 702 is recognized as a good credit score. While different scoring models might yield slightly different scores, checking a VantageScore 3.0 can provide a reasonable estimate of a VantageScore 4.0, as they are fundamentally similar.

Glossary:

- Credit Score Ecosystem: The network of entities, models, and practices involved in assessing and assigning credit scores, including credit bureaus, scoring companies (like FICO and VantageScore), and lenders.

- Credit Score Competition Act (2018): A law signed by President Trump that established the use of modern credit scoring models for mortgages sold to Government-Sponsored Enterprises (GSEs).

- Credit Utilization Rate: The amount of available credit that a consumer uses, typically expressed as a percentage. It is a significant factor in credit score calculations.

- Equifax: One of the three major nationwide consumer reporting agencies (credit bureaus) in the United States, responsible for collecting and maintaining credit information.

- Experian: One of the three major nationwide consumer reporting agencies (credit bureaus) in the United States, responsible for collecting and maintaining credit information.

- Fannie Mae: A government-sponsored enterprise (GSE) that provides liquidity and stability to the mortgage market by purchasing mortgages from lenders.

- Fair Isaac Corporation (FICO): A data analytics company best known for its credit scoring system, which has historically dominated the mortgage underwriting process.

- Federal Housing Finance Agency (FHFA): The independent federal agency that regulates and oversees Fannie Mae, Freddie Mac, and the 11 Federal Home Loan Banks.

- Freddie Mac: A government-sponsored enterprise (GSE) that provides liquidity and stability to the mortgage market by purchasing mortgages from lenders.

- Government-Sponsored Entities (GSEs): Financial services corporations created by the U.S. Congress to enhance the flow of credit to targeted sectors of the economy, such as housing (e.g., Fannie Mae and Freddie Mac).

- Machine Learning: A type of artificial intelligence that allows computer systems to learn from data without explicit programming, used by VantageScore 4.0 to score consumers with minimal credit histories.

- Mortgage Originations: The process by which a borrower applies for a mortgage loan, and a lender processes that application.

- National Mortgage Professional (NMP): A publication and news source covering the mortgage industry, providing news, analysis, and data.

- Thin File Borrowers: Consumers with limited credit history, making it difficult for traditional credit scoring models to assess their creditworthiness. VantageScore 4.0 aims to address this.

- Trended Data: Credit data that reflects patterns in borrower behavior over time, rather than just a single point in time. VantageScore 4.0 incorporates up to two years of trended data.

- Tri-merge Credit-Scoring Model: A credit report or scoring model that combines credit data from all three major credit bureaus (Experian, Equifax, and TransUnion) into a single report.

- TransUnion: One of the three major nationwide consumer reporting agencies (credit bureaus) in the United States, responsible for collecting and maintaining credit information.

- VantageScore 4.0: One of the latest credit scoring models developed by Experian, TransUnion, and Equifax, designed to be more inclusive and use advanced data analysis.

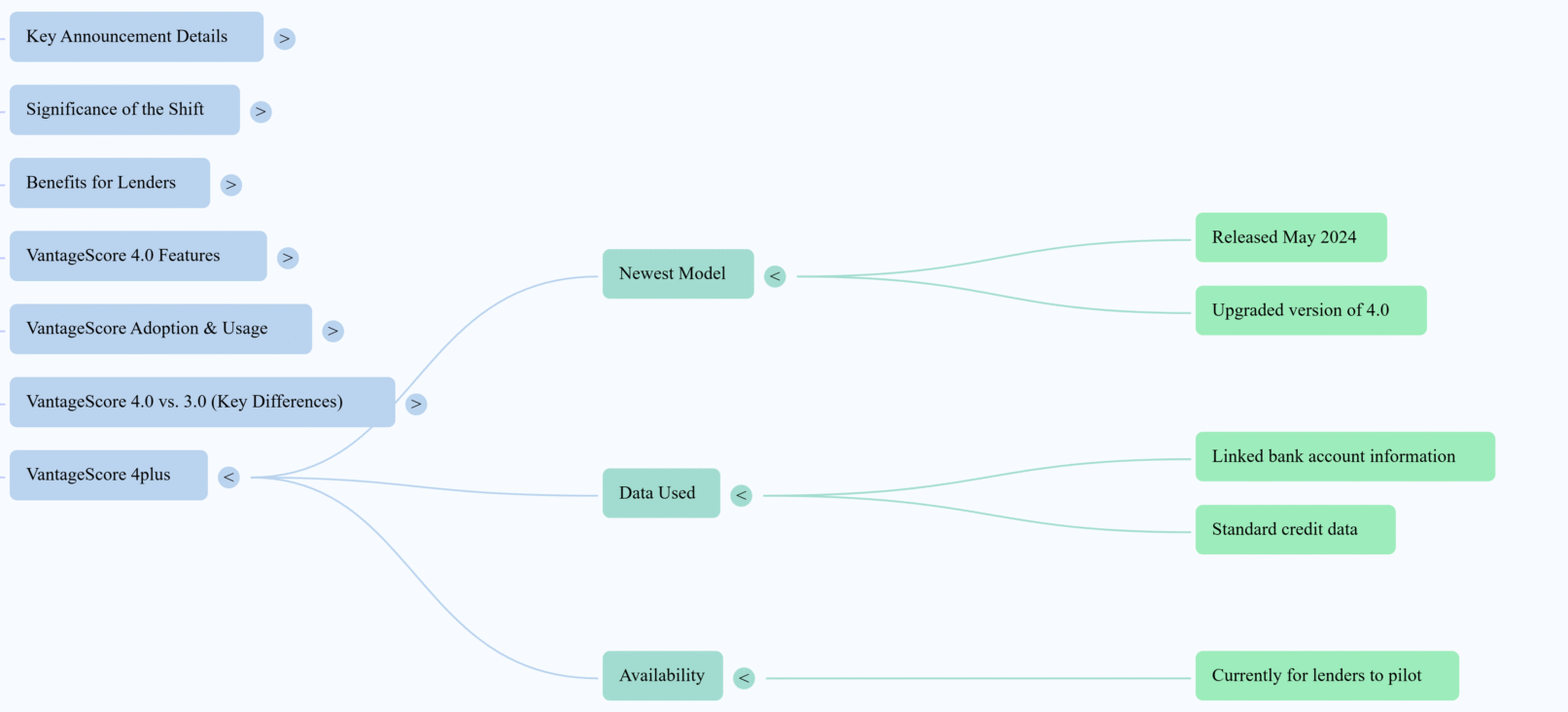

- VantageScore 4plus: The newest credit scoring model from VantageScore (released May 2024), which uses consumers’ linked bank account information in addition to standard credit data.

- William J. Pulte: The Director of the Federal Housing Finance Agency (FHFA) who announced the allowance of VantageScore 4.0 for Fannie Mae and Freddie Mac mortgages.

Cast Of Characters:

- William J. Pulte: Current Director of the Federal Housing Finance Agency (FHFA). He is a key figure in the decision to allow lenders to use VantageScore 4.0 for Fannie Mae and Freddie Mac mortgages, expressing a focus on increasing competition, lowering costs, and expanding credit access to “forgotten Americans.” He is active on X (formerly Twitter) in announcing these policy changes and vocal about his views on the financial system and the previous administration.

- Silvio Tavares: President and CEO of VantageScore. He praises Director Pulte’s decision, stating it will “revolutionize the American mortgage market” and provide homeownership opportunities to millions.

- Donald J. Trump: Former President of the United States. He is credited by Director Pulte for a “landslide mandate to lower costs” and for signing the 2018 Credit Score Competition Act, which laid the groundwork for modern credit scoring models in GSE mortgages. Pulte refers to him as “my boss, POTUS” in a July 8, 2025 post.

- Jeff Richardson: Vice President of Marketing and Communications for VantageScore. He provides insight into how the VantageScore 4.0 model’s use of “trended data” might advantage certain borrowers.

- Jerome Powell: Chairman of the Federal Reserve. He is mentioned in the sources as being targeted by FHFA Director Pulte for an investigation, with Pulte alleging he lied in testimony and should be fired.

- Ola Fadahunsi: VantageScore Media Contact.

- Lauren Schwahn: Senior Writer & Content Strategist at NerdWallet, specializing in personal finance, debt, credit scoring, and budgeting.

- Sheri Gordon: Former Assigning Editor on the Core Personal Finance team at NerdWallet, with expertise in credit scoring, budgeting, and money-saving.

- Louis DeNicola: Personal finance writer and contributing writer at Intuit Credit Karma, who has written for American Express, Discover, and Nova Credit.

Podcast:

| Our Loan Programs Video Resources |

Agent Branded Website View Example Get Your Branded Site |

![]()

|

|